In this multi-part series of press announcements, we dissect drivers of currency phenomena, including: i) interest rate perceptions, ii) current account intricacies and the real economy, iii) capital flow dynamics in the financial account, and iv) money supply theories in relation to debt levels and the fiscal position. In this first part, we discuss the impact of interest rates on currency sentiment.

Interest rate differentials remain a significant concern for the ringgit, reflecting historic shifts in global interest rate expectations led by the US. Differentials in interest rates between advanced economies’ currencies against those of emerging economies contributed to an extended depreciation of the latter’s currencies, leading to spillover effects on Malaysia’s foreign exchange reserves.

A common underlying issue affecting the ringgit is the perception of interest rate differentials. Essentially, international portfolio funds tend to flow from lower interest rate regimes to higher interest rate regimes due to yield-seeking behaviour. The median interest rate is 9.25% in the actively traded capital markets of the Americas; 5.25% in Europe, the Middle East, and Africa (EMEA); and 3.50% in the Asia Pacific. Malaysia’s policy interest rate currently stands at 3.00%. Of the 32 countries in this sample space, the median interest rate is 5.10%. While Malaysia seems to have relatively low interest rates, it is noteworthy that among the 32 countries in the sample space, Malaysia is one of only three countries not expected to cut interest rates over the next 12 months. This presents a positive counterweight narrative to Malaysia’s comparatively low interest rates. That said, the market’s expectation of stable interest rates in Malaysia, in contrast to rate cuts in most other countries, suggests that Malaysia’s current interest rate is a result of interest rate normalisation. Unlike in other countries, interest rates in Malaysia have increased only moderately in recent years. Furthermore, the present monetary policy is described as supportive by Malaysia’s central bank.

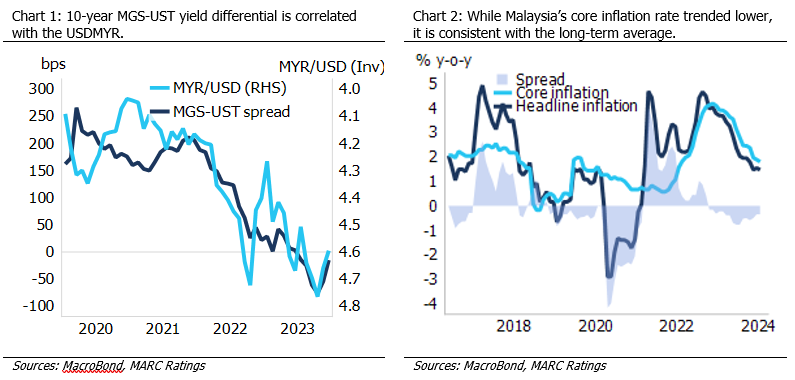

In relation to interest rate prospects, the monetary policy position for a central bank at any given time can be assessed as either hawkish, neutral, or dovish, with hawkish rhetoric leaning towards higher interest rates leading to currency appreciation. Conversely, dovish statements lead to currency depreciation. Whether correctly or incorrectly, Malaysia’s present supportive monetary policy may be construed as accommodative or dovish, especially in relation to higher interest rates in several other economies. As a proxy of the realised impact of interest rate expectations, the 10-year Malaysian Government Securities (MGS) to 10-year US Treasury (UST) yield differential declined from a positive 117 basis points (bps) in February 2019 to negative 39 bps in February 2024; during this time, the ringgit depreciated from RM4.07 to RM4.75.

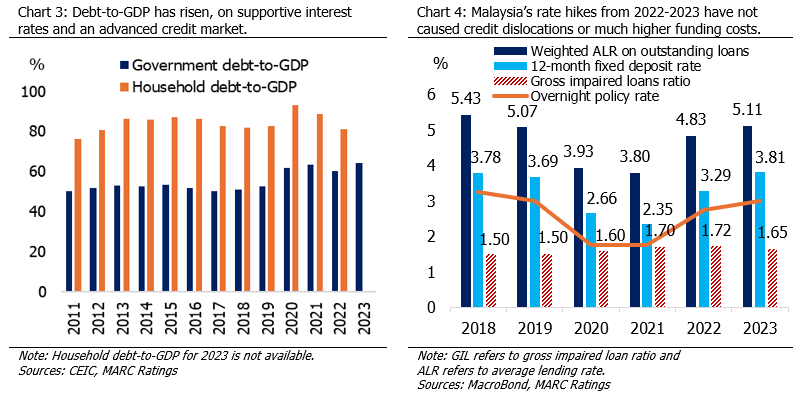

Regardless of any actual change or maintenance of the interest rate, the interest rate policy could be strategically communicated such that it highlights Malaysia’s strong fundamentals and expresses the retention of policy flexibility, without hinting at an accommodative policy. Indeed, Malaysia’s robust economy provides the country policy versatility over the direction and level of future interest rates. For example, while inflation has dropped over time, Malaysia’s core inflation rate is not low and is consistent with the long-term average, with the potential for upward pressures as subsidies are rationalised. Furthermore, Malaysia’s healthy banking system and its sound credit quality is sufficient to withstand an increase in the policy rate. Contrary to common perception, the increase in the interest rate by 125 bps to 3.00% in 2023 from 1.75% in 2022 did not result in a rise in loan impairments. Throughout this period, the gross impaired loans (GIL) ratio remained very low and declined from the peak of 1.85% in June 2022 to 1.65% as at January 2024.

Another consideration is whether a preference for borrowings over a preference for savings occurred due to low interest rates, and if this affords further policy flexibility to raise interest rates. In Malaysia, gross savings as a share of gross domestic product (GDP) dropped to 26.6% in 2022 from 32.7% in 2002. Consequently, the household debt-to-GDP ratio rose to 81.0% in 2022 from 67.2% in 2002. Relatedly, low interest rates depress returns to both domestic and international investors, which adversely impacts net pension funding positions and retirement savings at the domestic level, while also discouraging international funds from flowing into Malaysia. While there are multiple factors affecting the level of savings and debt, interest rates present a policy option to influence preferences towards borrowings and savings.

Monetary macroeconomics and exchange rates are not only functions of interest rates, or the price of money, but also the supply of money. Easy monetary policy is inimical to fiscal consolidation. Low interest rates may encourage a tendency towards an expansionary fiscal policy and a fiscal deficit which, in turn, will raise money supply, lower the price of money, and cause depreciation pressures on a currency. Plans have been made in Malaysia to contain and lower the fiscal deficit over time. However, the financial market’s — including the ringgit’s — reaction to these measures depends on the management of expectations, including the ability to meet or exceed originally planned targets on GDP growth and the fiscal balance-to-GDP ratio. Further information on aspects of structural reform can be found here.

Apart from interest rate differentials influencing the exchange rate, capital flows and non-financial market flows, particularly those stemming from the trade sector, play a major role in influencing the value of the exchange rate over the long term.

This press announcement is the first in a multi-part series enumerating our opinions over the ringgit’s pathway and accompanying adjustments that can potentially be made to better align the value of the ringgit, such that it reflects Malaysia’s solid fundamentals.