The year 2026 has thus far been defined by escalating geopolitical instability. Following US intervention in Venezuela and the capture of its president, a more systemic shock emerged. On 28 February, the US and Israel launched coordinated strikes against Iran, and Tehran retaliated with attacks on US military outposts across the Middle East.

Hostilities remain ongoing, while additional US military assets to the region remain in transit, suggesting additional phases to the conflict. Additionally, Tehran has ruled out ceasefire negotiations while US and Israeli strikes continue, and Iranian leaders have signalled the possibility of escalating retaliation across the region.

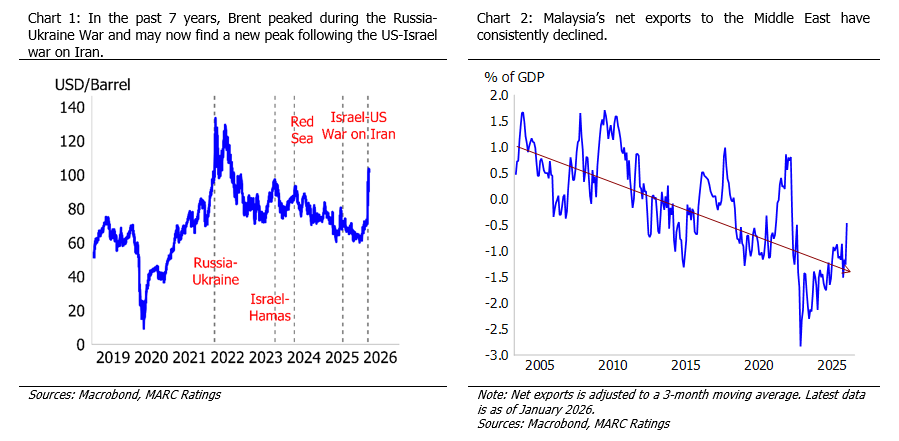

Disruptions to the Strait of Hormuz, which handles around a fifth of global oil supply, have effectively closed the chokepoint and caused Brent crude to exceed USD100 per barrel (USD/bbl). To ameliorate the situation, the International Energy Agency has coordinated the largest strategic petroleum reserve release in history, amounting to approximately 400 million barrels of oil from member countries. However, this would only serve as a temporary shock absorber and energy prices will likely retain a geopolitical risk premium, even though underlying supply surpluses may eventually moderate prices. Furthermore, the restoration of damaged oil infrastructure is likely to be gradual, constraining the pace at which supply conditions normalise. MARC Ratings now expects Brent crude to average between USD70/bbl and USD80/bbl in 2026, revised upwards from the earlier forecast range of USD60/bbl to USD70/bbl.

For Malaysia, the impacts of the conflict are expected to be mild given minimal trade exposure to the Middle East and Malaysia’s position as a net exporter of hydrocarbons. Malaysia’s trade is skewed towards Asia, anchored by robust exports in electrical and electronics (E&E), machinery, and palm oil products. Drawing parallels during the immediate effects of the Russia-Ukraine War, with Brent averaging above USD100/bbl, Malaysia’s overall exports still managed to grow substantially. However, domestic inflation, particularly within the transport segment, will face upward pressure. While RON95 petrol remains shielded by government subsidies, diesel and jet fuel prices are market-linked, which may raise transportation costs, leading to secondary inflation across broader consumer segments. Nevertheless, given that the transport component accounts for about a tenth of Malaysia’s aggregate Consumer Price Index basket, the overall impact on headline inflation is expected to remain manageable, especially with Malaysia’s targeted subsidies. As such, Malaysia’s inflation rate may rise, but remain contained at around 2% in 2026. Fiscally, due to potentially higher subsidies, the fiscal deficit-to-GDP ratio may rise but remain healthy at below 4% in 2026, subject to possible cuts in other expenses and increases in revenue sources such as contributions by government-related entities.

Key domestic industries, namely E&E, chemicals, agriculture, and logistics, will face immediate exposure to elevated input costs, particularly for refined petroleum and fertilisers. Simultaneously, potential trade diversion bodes well for Malaysian liquefied natural gas exporters and the crude palm oil sector, where the latter stands to gain from accelerated biofuel demand on higher oil prices. Balancing external geopolitical events with domestic economic resilience, MARC Ratings expects GDP to remain robust, with downside risk of 0.2%-0.4% to our baseline 2026 GDP forecast of 4.6% for Malaysia, subject to the extent of the war in the Middle East.

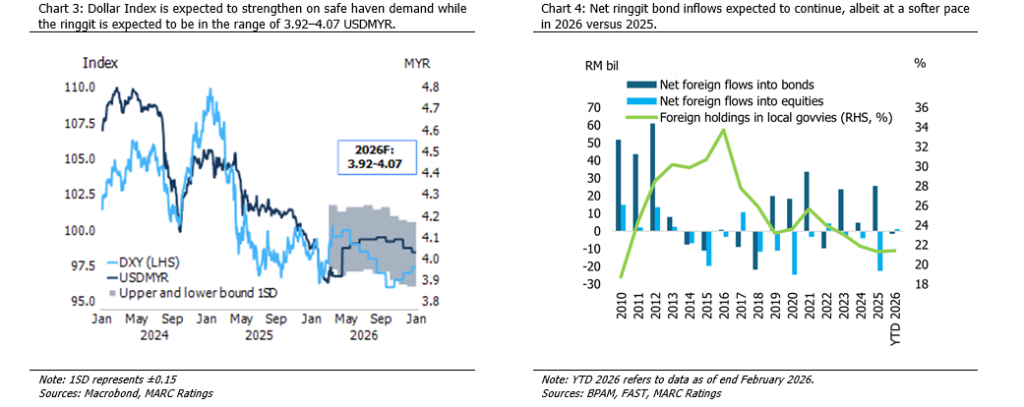

Additionally, MARC Ratings has widened the short-term ringgit forecast to 3.92-4.07 USDMYR from 3.88-3.98 USDMYR previously, reflecting heightened risk aversion affecting emerging market currencies and reduced expectations for US Federal Funds Rate cuts. Our forecasts incorporate the expectation that foreign bond inflows may moderate in 2026, compared to 2025, while noting Malaysia’s low sensitivity to episodic geopolitical shocks. For example, in 1Q2025, the Geopolitical Risk Index (GPR) surged by approximately 23.2% q-o-q, yet Malaysia recorded RM3.3 billion in net bond inflows (4Q2024: -RM13.9 billion). In 2Q2025, a further 26.6% q-o-q increase in GPR coincided with inflows of RM18.2 billion.

MARC Ratings opines that Bank Negara Malaysia may maintain the Overnight Policy Rate at 2.75% through 2026, on the balance of heightened external risks affecting growth and potentially higher inflation. In the US, interest rate expectations have shifted from two rate cuts prior to the war, to no rate cuts in 2026 due to the outlook for higher inflation. Nonetheless, the rise in the US unemployment rate to around 4.4% in 2025 from 3.5% in 2022, suggests that interest rate easing may re emerge after geopolitical pressures ease. Against this backdrop, we project the 10 year Malaysian Government Securities yield to find equilibrium at 3.55%-3.60% in the short term, up from the 2026 full year forecast of 3.35%–3.40% previously.

Notwithstanding these scenario analyses, the geopolitical landscape remains highly fluid. Military developments in the Middle East continue to evolve rapidly, and the conflict’s duration, geographic scope, and supply chain impacts remain uncertain. Consequently, market conditions, energy prices, and global financial sentiment may adjust swiftly as new information emerges. Looking forward, Malaysia’s structural economic trajectory remains robust and is well-positioned to recover strongly following the present phase of geopolitical dislocation in the Middle East, which will likely be transient. Strong domestic demand, steady growth dynamics, structural reforms and a diversified economy continue to support positive long-term prospects in Malaysia.